Wednesday, 20 January 2016

If you wish to know the answer for this question, then I'm sorry because I am also looking for it.

We know that when MYR value drops, exporters that sell their products or services in foreign currencies will get a profit boost.

However, if the raw material cost are denominated in foreign currencies and it makes up a big portion of its overall cost, then weakening MYR might not give too significant increase in profit.

If the export company has lots of debts/borrowings denominated in foreign currencies, then weakening of MYR might not be good for them.

In a company's quarterly financial report, it will show how its profit before tax are arrived at, either below the income statement or in the explanatory notes.

This section will usually include some realized/unrealized foreign exchange gain/loss.

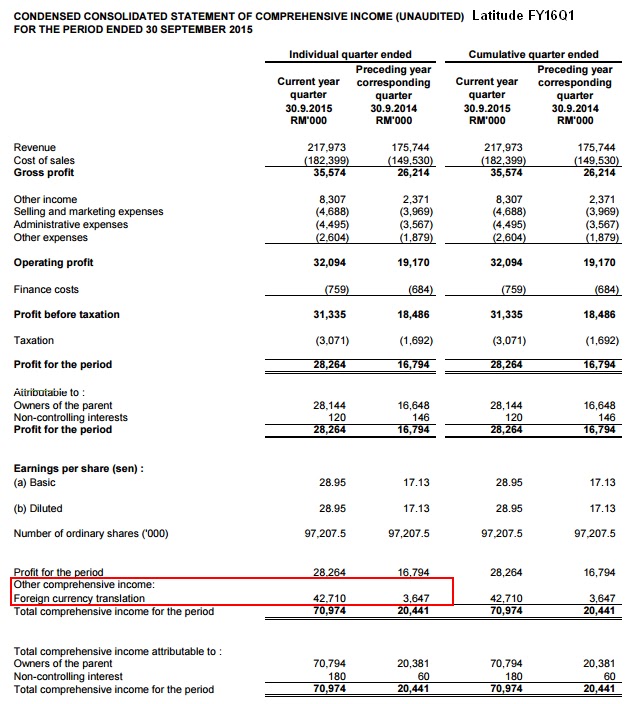

For example, in Latitude latest FY16Q1 quarterly report:

It shows that in FY16Q1, Latitude has a net forex gain of RM7.829mil, and these are already included in arriving at the net profit.

(1) What does this foreign exchange gain made up of?

I'm actually not sure and hope that someone with accounting knowledge can help to explain.

From my guess, this forex gain/loss should be from its receivables/payables, cash/debts denominated in foreign currencies and perhaps other items in the balance sheet.

For example, company Z exports its products in USD.

Lets say credit sales of USD100k is made at exchange rate of RM3.50 in early Q1. This means that a revenue of RM350k is registered and it will have USD100k as trade receivables.

In the middle of Q1, part of the bill USD40k (receivables) is settled at exchange rate of RM4.00. So there is a realized forex gain of 40k x RM0.50 = RM20k.

If other outstanding amount are not yet paid and MYR ends Q1 at RM4.30, then there will be an unrealized forex gain of 60k x RM0.80 = RM48k.

So the total forex gain for this particular sales is RM68k in Q1, which means that the company can potentially receive RM418k from a sales that worth RM350k.

The same should apply to payables in foreign currencies.

For borrowings, if a company secured USD100k borrowings at exchange rate of RM3.50, and it repaid USD30k at exchange rate of RM4.00, it will have a realized foreign exchange loss of RM15k.

If MYR ends the reporting quarter at RM4.30, then there will be an unrealized forex loss of RM56k.

Am I right?

However, (2) Which exchange rate is used as reference in the subsequent quarter? Is it the rate when sales are made, or the rate at end of previous quarter?

Lets use the company Z mentioned earlier as example.

Company Z makes USD100k sales in early Q1 at RM3.50 rate, and ends Q1 with USD60k receivables at RM4.30 rate. If the bill is settled fully in Q2 at exchange rate of RM4.10, will it register a realized forex gain of 60k x RM(4.10 - 3.50) = RM36k in Q2?

Or for Q2, we use the exchange rate at end of Q1 which is RM4.30 as a reference so company Z will register forex loss of 60k x RM(4.10 - 4.30) = -RM12k when the rate drops from RM4.30 to RM4.10?

Besides, there is another "foreign currency translation" profit in the income statement under "other comprehensive income".

For Latitude in the same quarter, the amount of foreign currency income is relatively huge at RM42.710mil in a single quarter.

(3) What does this foreign currency translation income made up of?

I think this should be for its foreign subsidiaries which is in Vietnam.

As Vietnam Dong also appreciates significantly against MYR, there will be forex gain but I'm not too sure how this number is derived from but it seems like it is from the increase in net assets of its foreign subsidiaries QoQ due to currency exchange rate changes.

From what I understand, this type of profit should not be included under profit attributable to shareholders but it should not be totally ignored so it is put under "other comprehensive income".

So, it will not contribute to the company's net profit and EPS.

Hopefully some expert will help to answer the questions marked in red above.

没有评论:

发表评论