Year-2011 Overview

(THP annual report 2011)

[Am Research 21.June.2012]

Statistics

- 大馬棕油局數據顯示,11月大馬原棕油產量走低10.8%至146萬公噸,但出口卻按月成長2.7%至150萬公噸,促使庫存從10月的179萬公噸下滑9%至164萬公噸,是繼7月的141萬公噸以來最低的庫存水平。

- 大馬原棕油庫存“跌跌”不休,供應吃緊憂慮死灰復燃,帶動原棕油價突破3千700令吉,創30個月新高,分析員相信疲憊產能和強勁出口將為強勢原棕油價帶來支撐,但隨市場供需在明年中恢復正常,第三波原棕油漲潮料告一段落。

- 益資利研究表示,疲憊產能和強勁出口、大豆油供應短缺,以及南美洲惡劣氣候影響大豆種植,將為強勢原棕油價帶來支撐。

- 但僑豐研究認為,拉妮娜效應對原棕油生產國影響未如預期嚴重,相信若現有親切氣候條件延續,產能旺季將從2011年6月或7月開始展開。

- 以前兩輪原棕油漲潮為期37個月為準,此番漲潮料可延續至2011年11月,但礙於產能旺季在年中開始,原棕油價上漲週期可能相對較短。

- 中國及印度目前是世上兩大棕油消費國,兩國的棕油消耗量在過去5年間平均每年分別上漲達5%及21%。其中,印度的棕油消耗量在經過今年的強勁增長後,目前更已較中國高出23%,達到775萬公噸。

同時,分析員指出,隨著印度與大馬將在明年簽訂自貿協定(FTA),相信屆時印度的棕油消費量還將更進一步上升,而預期大馬明年的棕油生產量僅將取得約5%的成長。

- 國內方面,政府的生化柴油政策預計將在明年6月施行,相信也將進一步刺激本地的棕油需求量。交易員透露,該項針對生化柴油燃料的B5標準標明,市場中售賣的柴油必須含有5%的生化柴油,而生化柴油的主要原料為原棕油,因此該項措施的落實相信將能夠帶動原棕油價格的上漲。事實上,該政策自2008年提出以來已二度遭到展延,因此分析員表示,並不能排除該計劃仍會再度遭到擱置。

- 中國目前仍是全球最大的食用油消費國,因此,若中國政府突然實施諸如提高原棕油進口關稅等措施,以保護當地業者,或將對全球的原棕油市場造成顯著的影響。

http://biz.sinchew.com.my/node/41899 (Year-2010)

- The average CPO price for 2009 is close to RM2,250 per metric tonne, approximately half of its peak level of RM4,480 per metric tonne in March 2008. Following the recovery of world economy, CPO prices are now trading at above RM3,500 per metric tonne level.

[JF Apex research Feb.2011]

- Datuk Zainal Azwar Zainal Aminuddin, executive director and CEO of TH Plantation, explained that a hectare of land in Kalimantan or Sumatera may cost US$450 to US$650 (RM1,341 to RM1,937). By comparison, the price range in Sabah is RM4,500 to RM6,000 per ha and RM4,000 to RM5,000 per ha in Sarawak.

http://www.theedgemalaysia.com/in-the-financial-daily/185795-th-plantations-to-acquire-land-in-indonesia.html (Year-2011)

[JF Apex research Feb.2011]

[JF Apex research Feb.2011]

- 12月原棕油生產按月挫8.2%,至149萬公噸,按年則增長21.3%。出口按月挫4.5%至159萬公噸,內需保持疲弱,進口按月增長66.2%、按年增長20.9%至15萬公噸。

- 興業研究說,最大進口國印度進口全球的17%產量,預測今年進口菜油將增長2.7%以增加庫存,這是以其國內菜油按年增長6%而定;不過若干旱來襲,進口量可能提高。

- “但印度的價格敏感度高,若大豆油折價大,將擴大進口原棕油,目前為230美元,對油菜籽油從上月280美元下調至240美元。儘管有收窄之勢,但原棕油、大豆油價差仍高於史上的100美元,原棕油、油菜籽油價差200美元,因此原棕油需求仍有上漲潛能。"興業研究。

- 至於消費全球16%棕油產量的中國,正增加菜油庫存以抑制通膨,去年下半年就增庫存。自去年下半年傾銷庫存協助抗通膨後,中國庫存按年減40%或只剩230萬公噸,不足一個月的消費。

http://biz.sinchew.com.my/node/55843 (Year-2011 Q4)

[OSK research 6.April.2012]

- Strategic land is hard to come by these days especially after the forest moratorium imposed by the Indonesian government in 2011. Land owners, in general, are also taking advantage of the present high CPO price to seek maximum land value.

[Maybank IB 16.April.2012]

- The local plantation industry has experienced a challenging and taxing episode for the year 2012. Based on the Malaysian Palm Oil Board (MPOB) statistic, the CPO production declined marginally by 0.7% to 18.79mil metric tonnes compared to 18.91mil MT in 2011.

- The national average of the Fresh Fruit Bunches (FFB) production per hectare(ha) weakened by 4.1% to 18.89MT (2011:19.69MT). The decrease was due to stress on the trees after experiencing high FFB production in 2011.

- Export earnings from palm oil and oil palm products have plunged by 11.2% to RM71.4bil from RM80.4bil in 2011 due to lower export prices despite the increase in export volume by 1.2% to 24.56mil MT (2011:24.27mil MT).

- According to MPOB, the closing stocks increased by 27.7% to 2.63mil MT from 2.06mil MT in 2011,mainly attributed to the high palm oil opening stocks and decline in palm oil exports by 2.4%.

- China maintained its position as the largest palm oil export market for the 11th consecutive year, followed by India, the EU, Pakistan,USA,Japan and Iran. These 7 markets combined accounted for 11.83mil MT or 67.4% of total Malaysian palm oil exports in 2012.

(THPlant Annual Report 2012)

- The plantation industry is currently facing labour shortage and failure to address this would be detrimental to the industry especially in the long run.

(THPlant Annual Report 2012)

[CIMB IB 15.Oct.2013]

- 大马政府去年制定的新版原棕油出口税2013年1月1日正式上路。在每月依据市场价格来计算出口税率的方式下,1月份的出口税率已被定为零税率。新版原棕油出口税改变游戏规则,分析员认为我国原棕油库存减低,将有机会使原棕油期货价格翻身。

- “这不但允许大马下游业者在对垒印尼竞争同行时拥有更大的竞争空间,也对大马高企的原棕油库存提供更大的出口途径。”

- 2012年11月录得256万公吨的历史记录后,我国原棕油库存将在今年上半回落。

http://www.nanyang.com/node/503083 (Year-2013 Q1)

- 大马2012年12月份棕油库存量创下连续四个月的新高水平,与市场早前的预期有出入,这是基于出口无法追上產量,库存新高导致期货价格走低。

- 大马棕油局数据显示,2012年12月库存量进一步提升2.4%,至262万公吨。去年11月的库存数据经调整之后,为256万公吨。

- 在上述数据公布前,基准棕油期货合约价格已下跌0.5%至2399令吉。原棕油3月期货全天跌29令吉,收在2383令吉,因库存持续走高让投资者感到忧心。

- 12月產量按月下跌5.8%至178万公吨,因季节性豪雨影响主要棕油种植地的收成。然而,由於12月的棕油出口也微跌0.7%至165万公吨,因此,无法降低库存量。大马出口下滑,是因为主要买家印度和中国目前正处冬季,而棕油在寒冷天气会结晶,因此中印的需求转向当地的油籽,此外,这两个地区的进口食用油库存量仍处高水平。

- 货柜调查公司Intertek数据显示,大马1月份首十天的棕油出口暴跌25%至37万3462公吨

http://www.orientaldaily.com.my/?option=com_k2&view=item&id=38434:12&Itemid=198 (Year-2013 Q1)

-印尼,考虑下调原棕油出口税对抗我国的竞争。印尼贸易部长吉塔维查万今日向媒体表示,只要能够有助于维持该国下游(棕油加工业者和炼油业者)的发展和竞争力,下调的幅度可以去到任何水平。

-我国(Malaysia)为了减低国内居高不下的棕油库存,在今年开始调降出口税,1月份为零。

- 根据印尼棕油生产商协会(GAPKI)今日公布数据,该国11月份棕油出口按月增长39%至198万公吨;累计11个月的出口量达1630万公吨,按年增长3.2%。该协会预测,2013年的棕油出口量可达2000万公吨,相较于2012年的1820万公吨(预测);而产量方面,则预期可达2800万公吨,按年增长5.7%。

http://www.nanyang.com/node/504057?tid=462 (Year-2013 Q1)

- Stockpile. Malaysia’s palm oil stockpile crept up to 2.63m MT at end-Dec 2012 (+2% MoM, +28% YoY) – comprising record CPO stocks of 1.58m MT (-6% MoM, +48% YoY) and processed palm oil stocks of 1.05m MT (+17% MoM, +6% YoY) – see Fig 10. The marginally higher inventory is mainly due to better-than-expected CPO production of 1.78m MT in Dec 2012 (-6% MoM, +19% YoY) and weaker domestic consumption (-39% MoM, +151% YoY) whilst exports were largely flattish (-1% MoM, +4% YoY).

- Refinery utilization rate. The positive take- away from this monthly statistics is affirmation that Malaysian refiners are regaining their competitiveness vis-à-vis Indonesian peers as refinery utilization rate improved to 76.4% in Dec 2012 against an average of 62% for Jan-Sep 2012 (see Fig 5). Since Sep 2012, Malaysian refiners have benefited from a MYR100/t “discounted” CPO ASP from the millers (especially in Sabah and Sarawak).

- Exports.Initial estimates of Malaysia’s Jan 1-10 palm oil exports by Intertek (ITS) and Societe Generale de Surveillance (SGS) is lower at 0.37m MT (-25% MoM) and 0.34m MT (-34% MoM) respectively. Besides seasonality factor, exports to China were down 58% MoM to 0.077m MT during the period. This is understandable as exporters are taking pre-cautionary measures ahead of China’s tighter food-safety measures which came into effect on 1 Jan 2013. Our view is that this is not a structural change in demand but a temporary hiccup as compliance can be achieved with better planning and marginally higher compliance costs.

[Maybank Investment Jan.2013]

- The tightness in supply of global 17 oils and fats with stock-to-usage ratio of 11.4% for the 2012/13F marketing year (2011/12: 12.3%) means that the world will rely on the ample palm oil stocks to satisfy global requirements.

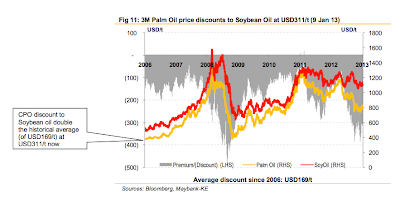

- Furthermore, the near-historically wide discounts of CPO prices relative to soybean oil (3M futures on 31 Dec 2012: USD309/t) and rapeseed oil (USD423/t) makes CPO extremely attractive.

- India and China are natural target market for CPO exports as India imposes a 7.5% import duty on refined palm oil but zero for CPO. Meanwhile, China imposes an import duty of 2% for CPO against 9% for edible oil. A boost of export will gradually reduce Malaysia's stock pile and boost CPO price.

- In July 2012, India reacted to Indonesia's tax reform by revising its benchmark import price for refined palm oil; effectively doubling import duty for refined palm oil to USD79/t (from USD36/t) back then. Fortunately, the Indian government has recently rejected a request by the Solvent Extractors Association of India to impose 10% import duty on CPO (currently tax free) and 20% on RBD palmolein (currently at 7.5%). The proposal to raise taxes was to help soybean farmers. Had the proposal been approved, this would have dampened demand for palm oil products in the near term. India is one of the world's largest consumers of palm oil at 6.6mil MT in 2010.

- China's Inspection and Quarantine Bureau has called for tougher quality measures on imported edible palm oil for the benefit of Chinese consumers come 1 Jan 2013. Palm oil shipments to China that do not meet the 2009 edible oils quality control specification on arrival at China ports (previously: shipped quality at origin) will be turned away. It seems "off-spec" shipment can no longer be re-fined at its shores. In essence, exporters/refiners are held responsible for the deterioration of oil quality during shipment. Officials from Malaysia Palm Oil Board (MPOB) was quoted as saying that approximately 95% of Malaysian edible oil exports to China meet China's stringent regulations (on arrival in China). The tougher measure imposed by China could slow down demand for refined palm oil in the short term given the uncertainties on its enforcement and as the industry adjusts to the new requirements.

- CPO price has traded at an average historical premium of USD208/t since 2006 over diesel price. Given the recent CPO price correction, CPO now trades near parity to diesel, a level not seen since end-2008. At this level, it is economically viable to produce and blend more palm biodiesel with fossil diesel wit little-to-no government subsidies.

- Europe Commission (EC) has approved the Roundtable on Sustainable Palm Oil (RSPO) scheme that would certify as sustainable transport fuel made from palm oil. This means palm biodiesel from sustainable sources qualify for subsidies and count towards the EU's renewable energy targets.

- In Malaysia, the nationwide roll-out of the B5 programme started on 1.June.2011 (after several years of delay) with the central region, covering Putrajaya, Malacca, Negeri Sembilan, Kuala Lumpur and Selangor. The programme in the central region utilises 0.112mil tonnes of CPO annually. By end-2012, Malaysia is ready to have a nationwide implementation of theB5 programme which the government hopes to raise consumption to about 0.5mil MT of palm oil annually. In Dec 2012, the Malaysia government eas reported to have agreed to implement the B10 programme (blending of 10% palm oil biodiesel with petroleum diesel) as a measure to help support failing CPO price. The latest measure will increase the consumption of CPO by another 0.3mil MT a year.

- In Oct 2012, the governors of eight states in the USA and almost 200 members of Congress asked the U.S Environment Protection Agency (EPA) to suspend rules that mandate production of ethanol for use in gasoline. EPA has since responded in Nov 2012 and turned down the request. A continuation of US biofuel mandate will ensure demand for bioethanol and biodiesel in the US to help sustain prices of corn and soybean, which has a positive carry on CPO price.

- The US Congress reintroduced the USD1 per gallon tax credit (RM860/t) for biodiesel as part of the comprehensive tax bill passed on 2.Jan.2013. The tax credit will be retroactively applied from 1.Jan.2012 and through the end of 2013. Recall that this biodiesel tax incentive was first introduced in 2005 which expired on 31.Dec.2011. With its reinstatement, the US National Biodiesel Board expects the tax incentive to promote expansion in biodiesel production in coming months, in line with the larger biodiesel admixture mandate of 1.28b gallons (or 4.5mil MT) in 2013. Note that soya oil covered 54%-55% of US biodiesel production in 2012. The reintroduction of this tax incentive will therefore boost US's import reliance of oils & fats in 2012/13 to satisfy domestic demand for food and non-food purposes.

- The plantation sector as implemented a RM650-RM850 per month minimum wage since 1.Sept.2011. On 1.May.2012, the Malaysian government announced a new minimum wage (effective 2013) at RM900 per month for Peninsular Malaysia and RM800 per month for East Malaysia. Minimum wage will have a marginal impact on the West Malaysia plantation players and a moderate impact on East Malaysian plantation players. Most if not all of the plantation workers are taking home more than RM1000 per month(inclusive of incentives and allowance) with some far exceeding the minimum wage.

- In end-Nov 2012, Indonesia's Ministry go Manpower also announced a minimum wage hike for 15(out of 33) provinces in Indonesia, ranging from a low of 8% to a high of 49%. Indonesia's minimum wage increase has averaged between 10-15% p.a. over the last few years. But hike for 2013 are phenomenal for some provinces especially East Kalimantan +49% YoY.

- This is a long term structural issue for Malaysian plantation estates in that Indonesia's rapid increase in minimum wages will continue to erode Malaysia's attractiveness as an employment destination for foreign workers. It is an open secret that plantation estates in Malaysia are already facing labour shortage (especially harvesters), and the industry is heavily reliant on foreign labour. Plantation estates in Malaysia will now find it even more difficult to retain and recruit Indonesian workers, especially estates in Sabah(as it borders East Kalimantan). This in turn will lead to an even higher wage bill for estates in Sabah over time.

[Maybank Investment Jan.2013]

- Malaysia's palm oil stockpile crept up to 2.63mil MT at end-deC 2012 (+2% MoM, +28% YoY), comprising record CPO stocks of 1.58mil MT (-6% MoM,+48% YoY) and processed palm oil stocks of 1.05mil MT(+17% MoM, +6% YoY).

- The marginally higher inventory is mainly due to better-than-expected CPO production of 1.78mil MT in Dec2012 (-6% MoM,+19% YoY) and weaker domestic consumption (-39% MoM,+151% YoY) whilst exports were largely flattish (-1% MoM,+4% YoY).

- Refinery utilisation rate improved to 76.4% in Dec2012 against an average of 62% for Jan-Sept2012.

[Maybank Investment Jan.2013]

[CIMB Research Jan.2013]

[CIMB Research Jan.2013]

- Palm oil is currently the cheapest edible oil in the market, enabling it to raise its market share. China, India and Pakistan are the three largest consumers of palm oil, taking up a combined 41% of global palm oil imports in 2011, based on statistics from the Oil World publication.

[CIMB Research Jan.2013]

- CPO spot price has fallen 37% from its peak of RM3,568/tonne in 2012 to a low of RM2,231/tonne (as at 31 Dec 12) due to slower-than-expected demand which led to record palm oil stocks in Malaysia.

[CIMB Research Jan.2013]

[CIMB Research Jan.2013]

- 印尼正修法限制新棕油公司的种植面积不得超过10万公顷,分析员认为,这会影响想要扩展业务至该国的种植公司(包括大马公司在内)。据报道,印尼正修订油棕种植相关法令,以限制新种植公司的种植面积在10万公顷。惟国有企业与合作社将可豁免,及新规定不会影响已拥有执照的种植公司。

http://www.nanyang.com.my/node/528470?tid=761 (April.2013)

- Indonesia, the world’s biggest palm oil producer, will spend at least US$2.7 billion to build crude palm oil (CPO) processing facilities until 2014 to further boost the country’s CPO production capacity, an executive from the palm oil producer association has said.

- The new facilities will boost Indonesia’s processing capacity to 39.46 million tons a year in 2014, which will comprise 30.9 million tons for refining and fractionation capacity, 4.22 million tons for oleochemical production capacity and 4.34 million tons for biodiesel manufacturing capacity of 4.34 million tons.

- In the first quarter of this year, investors have spent around $1.02 billion on new processing facilities. The new investments are expected to increase the country’s total processing capacity to 30.9 million tons a year by year’s end, a 19.31 percent increase from the past year. The total processing capacities aimed for this year will consist of 25.1 million tons a year for refining and fractionation, up 24.88 percent from last year, about 2.2 million a year for oleochemical production and about 3.6 million tons a year for biodiesel manufacturing.

- Local industry players have said that the inflow of such sizeable investments was attributed to the government’s decision to change the export tax structure in late 2011, which effectively makes investments in the downstream industry more attractive. The new tax structure generates a margin of export tax on crude palm oil and downstream products, such as RBD palm olein of between 5.5 percent and 9.5 percent, making Indonesian products more competitive than those produced by Malaysian producers. Under the new tax regime, the export tax on processed palm oil products declines from 25 percent to 10 percent.

http://www.thejakartapost.com/news/2013/06/10/investors-spend-more-palm-oil-refineries.html (June.2013)

http://www.indexmundi.com/commodities/?commodity=palm-oil&months=60

http://www.palmoilhq.com/crude-palm-oil-cpo-futures/

- 提炼FFB = 得到 CPO & PK吗? 对。

- FFB的价钱,是根据 20% 的cpo 和 4% 的pk计算出来的,这个公式是自己发明的。如果要拿到这个价钱,必须是大公司。对于小园主来说, 要扣除暴利税, 东海岸价格更低, 厂商要求milling margin ,因此FFB收购价较低。http://bepi.mpob.gov.my/index.php/statistics/price/daily.html

http://www.investalks.com/forum/viewthread.php?tid=3544&highlight=tdm #15 tcs

- 四十年来,棕油在食油市场所占的份额,由5%到目前的超过40%,证明其优越性。在世界人口日增,各国日益富庶(食油消耗量与国民生产总值同步增长)及用途日广的趋势下,棕油前景亮丽。

http://www.nanyang.com/node/360888 (Year-2010)

- 最新的園丘行情,也反映出上述情況。數據顯示,樹齡9至18年的園丘平均價為每公頃4萬9千143令吉,平均產量是每公頃14公噸;至於樹齡4至9年的園丘,平均價格和產量分別是4萬5千920令吉和10公噸。

- 分析員指出,這些情況顯示,即使部份園丘的產量不高,只要地點適中,投資者依然願意出高價搶購,他們顯然不介意較低的短期回酬,而著重於長遠的利益。

http://biz.sinchew.com.my/node/55654 (Year-2011)

油棕种下后第三年就被列为“成熟”树,实际上还是没钱赚,要到第五年才略有盈利,这还要看原棕油的价格而定。

由第五年到第廿五年,盈利不断,但盛产期是由第七年至第十七年之间的十年,产量最高,如果原棕油价格挺秀的话,园主必然捞得盆满钵满,故园主对7-17最有好感。

由第十八年起,产量已开始走下坡;到第廿三年时已是树老叶黄,产量不多,到了要翻种的树龄。但是,如果原棕油价格奇高,像目前这样的话,园主也会拖延翻种,尽量利用其剩余价值,到第廿五年才翻种。

http://www.investalks.com/forum/viewthread.php?tid=3544&extra=&page=17 #330 wedals

Video

Useful sites:

http://www.palmoil.tv

http://www.palmoilhq.com

http://bepi.mpob.gov.my

http://econ.mpob.gov.my

Statistics

- 大馬棕油局數據顯示,11月大馬原棕油產量走低10.8%至146萬公噸,但出口卻按月成長2.7%至150萬公噸,促使庫存從10月的179萬公噸下滑9%至164萬公噸,是繼7月的141萬公噸以來最低的庫存水平。

- 大馬原棕油庫存“跌跌”不休,供應吃緊憂慮死灰復燃,帶動原棕油價突破3千700令吉,創30個月新高,分析員相信疲憊產能和強勁出口將為強勢原棕油價帶來支撐,但隨市場供需在明年中恢復正常,第三波原棕油漲潮料告一段落。

- 益資利研究表示,疲憊產能和強勁出口、大豆油供應短缺,以及南美洲惡劣氣候影響大豆種植,將為強勢原棕油價帶來支撐。

- 但僑豐研究認為,拉妮娜效應對原棕油生產國影響未如預期嚴重,相信若現有親切氣候條件延續,產能旺季將從2011年6月或7月開始展開。

- 以前兩輪原棕油漲潮為期37個月為準,此番漲潮料可延續至2011年11月,但礙於產能旺季在年中開始,原棕油價上漲週期可能相對較短。

- 中國及印度目前是世上兩大棕油消費國,兩國的棕油消耗量在過去5年間平均每年分別上漲達5%及21%。其中,印度的棕油消耗量在經過今年的強勁增長後,目前更已較中國高出23%,達到775萬公噸。

同時,分析員指出,隨著印度與大馬將在明年簽訂自貿協定(FTA),相信屆時印度的棕油消費量還將更進一步上升,而預期大馬明年的棕油生產量僅將取得約5%的成長。

- 國內方面,政府的生化柴油政策預計將在明年6月施行,相信也將進一步刺激本地的棕油需求量。交易員透露,該項針對生化柴油燃料的B5標準標明,市場中售賣的柴油必須含有5%的生化柴油,而生化柴油的主要原料為原棕油,因此該項措施的落實相信將能夠帶動原棕油價格的上漲。事實上,該政策自2008年提出以來已二度遭到展延,因此分析員表示,並不能排除該計劃仍會再度遭到擱置。

- 中國目前仍是全球最大的食用油消費國,因此,若中國政府突然實施諸如提高原棕油進口關稅等措施,以保護當地業者,或將對全球的原棕油市場造成顯著的影響。

http://biz.sinchew.com.my/node/41899 (Year-2010)

- The average CPO price for 2009 is close to RM2,250 per metric tonne, approximately half of its peak level of RM4,480 per metric tonne in March 2008. Following the recovery of world economy, CPO prices are now trading at above RM3,500 per metric tonne level.

[JF Apex research Feb.2011]

- Datuk Zainal Azwar Zainal Aminuddin, executive director and CEO of TH Plantation, explained that a hectare of land in Kalimantan or Sumatera may cost US$450 to US$650 (RM1,341 to RM1,937). By comparison, the price range in Sabah is RM4,500 to RM6,000 per ha and RM4,000 to RM5,000 per ha in Sarawak.

http://www.theedgemalaysia.com/in-the-financial-daily/185795-th-plantations-to-acquire-land-in-indonesia.html (Year-2011)

- 12月原棕油生產按月挫8.2%,至149萬公噸,按年則增長21.3%。出口按月挫4.5%至159萬公噸,內需保持疲弱,進口按月增長66.2%、按年增長20.9%至15萬公噸。

- 興業研究說,最大進口國印度進口全球的17%產量,預測今年進口菜油將增長2.7%以增加庫存,這是以其國內菜油按年增長6%而定;不過若干旱來襲,進口量可能提高。

- “但印度的價格敏感度高,若大豆油折價大,將擴大進口原棕油,目前為230美元,對油菜籽油從上月280美元下調至240美元。儘管有收窄之勢,但原棕油、大豆油價差仍高於史上的100美元,原棕油、油菜籽油價差200美元,因此原棕油需求仍有上漲潛能。"興業研究。

- 至於消費全球16%棕油產量的中國,正增加菜油庫存以抑制通膨,去年下半年就增庫存。自去年下半年傾銷庫存協助抗通膨後,中國庫存按年減40%或只剩230萬公噸,不足一個月的消費。

http://biz.sinchew.com.my/node/55843 (Year-2011 Q4)

[OSK research 6.April.2012]

- We deem the acquisition price of the planted area to be on the high side given that the total cost of planting (including land) to maturity in Indonesia should be between RM20,000 - RM25,000/ha (or USD6,667 – 8,333/ha).

- Strategic land is hard to come by these days especially after the forest moratorium imposed by the Indonesian government in 2011. Land owners, in general, are also taking advantage of the present high CPO price to seek maximum land value.

[Maybank IB 16.April.2012]

- 一旦收购完成(JV Co),云顶种植总地段將提高44.9%(或7万4千390公顷),超越IOI集团(IOICORP,1961,主板种植组)的总地段17万9千974公顷,成为第三大的种植公司,仅次於森那美(SIME,4197,主板贸服组)和吉隆坡甲洞(KLK,2445,主板种植组),分別达87万3千222和25万零729公顷。

http://biz.sinchew.com.my/node/59252 (Year-2012 Q2)

- Palm oil is the world's leading edible oil, accounting for 56% and 26% of oils and fats trading and consumption respectively in 2011.

http://biz.thestar.com.my/news/story.asp?file=/2012/12/4/business/12407543&sec=business (Year-2012 Q3)- Palm oil is the world's leading edible oil, accounting for 56% and 26% of oils and fats trading and consumption respectively in 2011.

- The local plantation industry has experienced a challenging and taxing episode for the year 2012. Based on the Malaysian Palm Oil Board (MPOB) statistic, the CPO production declined marginally by 0.7% to 18.79mil metric tonnes compared to 18.91mil MT in 2011.

- The national average of the Fresh Fruit Bunches (FFB) production per hectare(ha) weakened by 4.1% to 18.89MT (2011:19.69MT). The decrease was due to stress on the trees after experiencing high FFB production in 2011.

- Export earnings from palm oil and oil palm products have plunged by 11.2% to RM71.4bil from RM80.4bil in 2011 due to lower export prices despite the increase in export volume by 1.2% to 24.56mil MT (2011:24.27mil MT).

- According to MPOB, the closing stocks increased by 27.7% to 2.63mil MT from 2.06mil MT in 2011,mainly attributed to the high palm oil opening stocks and decline in palm oil exports by 2.4%.

- China maintained its position as the largest palm oil export market for the 11th consecutive year, followed by India, the EU, Pakistan,USA,Japan and Iran. These 7 markets combined accounted for 11.83mil MT or 67.4% of total Malaysian palm oil exports in 2012.

(THPlant Annual Report 2012)

- The plantation industry is currently facing labour shortage and failure to address this would be detrimental to the industry especially in the long run.

(THPlant Annual Report 2012)

- Market share of refining capacity in Malaysia

[CIMB IB 15.Oct.2013]

- 大马政府去年制定的新版原棕油出口税2013年1月1日正式上路。在每月依据市场价格来计算出口税率的方式下,1月份的出口税率已被定为零税率。新版原棕油出口税改变游戏规则,分析员认为我国原棕油库存减低,将有机会使原棕油期货价格翻身。

- “这不但允许大马下游业者在对垒印尼竞争同行时拥有更大的竞争空间,也对大马高企的原棕油库存提供更大的出口途径。”

- 2012年11月录得256万公吨的历史记录后,我国原棕油库存将在今年上半回落。

http://www.nanyang.com/node/503083 (Year-2013 Q1)

- 大马2012年12月份棕油库存量创下连续四个月的新高水平,与市场早前的预期有出入,这是基于出口无法追上產量,库存新高导致期货价格走低。

- 大马棕油局数据显示,2012年12月库存量进一步提升2.4%,至262万公吨。去年11月的库存数据经调整之后,为256万公吨。

- 在上述数据公布前,基准棕油期货合约价格已下跌0.5%至2399令吉。原棕油3月期货全天跌29令吉,收在2383令吉,因库存持续走高让投资者感到忧心。

- 12月產量按月下跌5.8%至178万公吨,因季节性豪雨影响主要棕油种植地的收成。然而,由於12月的棕油出口也微跌0.7%至165万公吨,因此,无法降低库存量。大马出口下滑,是因为主要买家印度和中国目前正处冬季,而棕油在寒冷天气会结晶,因此中印的需求转向当地的油籽,此外,这两个地区的进口食用油库存量仍处高水平。

- 货柜调查公司Intertek数据显示,大马1月份首十天的棕油出口暴跌25%至37万3462公吨

http://www.orientaldaily.com.my/?option=com_k2&view=item&id=38434:12&Itemid=198 (Year-2013 Q1)

-印尼,考虑下调原棕油出口税对抗我国的竞争。印尼贸易部长吉塔维查万今日向媒体表示,只要能够有助于维持该国下游(棕油加工业者和炼油业者)的发展和竞争力,下调的幅度可以去到任何水平。

-我国(Malaysia)为了减低国内居高不下的棕油库存,在今年开始调降出口税,1月份为零。

- 根据印尼棕油生产商协会(GAPKI)今日公布数据,该国11月份棕油出口按月增长39%至198万公吨;累计11个月的出口量达1630万公吨,按年增长3.2%。该协会预测,2013年的棕油出口量可达2000万公吨,相较于2012年的1820万公吨(预测);而产量方面,则预期可达2800万公吨,按年增长5.7%。

http://www.nanyang.com/node/504057?tid=462 (Year-2013 Q1)

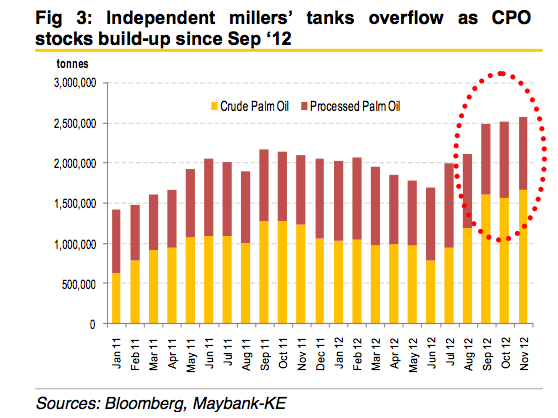

- Stockpile. Malaysia’s palm oil stockpile crept up to 2.63m MT at end-Dec 2012 (+2% MoM, +28% YoY) – comprising record CPO stocks of 1.58m MT (-6% MoM, +48% YoY) and processed palm oil stocks of 1.05m MT (+17% MoM, +6% YoY) – see Fig 10. The marginally higher inventory is mainly due to better-than-expected CPO production of 1.78m MT in Dec 2012 (-6% MoM, +19% YoY) and weaker domestic consumption (-39% MoM, +151% YoY) whilst exports were largely flattish (-1% MoM, +4% YoY).

- Refinery utilization rate. The positive take- away from this monthly statistics is affirmation that Malaysian refiners are regaining their competitiveness vis-à-vis Indonesian peers as refinery utilization rate improved to 76.4% in Dec 2012 against an average of 62% for Jan-Sep 2012 (see Fig 5). Since Sep 2012, Malaysian refiners have benefited from a MYR100/t “discounted” CPO ASP from the millers (especially in Sabah and Sarawak).

- Exports.Initial estimates of Malaysia’s Jan 1-10 palm oil exports by Intertek (ITS) and Societe Generale de Surveillance (SGS) is lower at 0.37m MT (-25% MoM) and 0.34m MT (-34% MoM) respectively. Besides seasonality factor, exports to China were down 58% MoM to 0.077m MT during the period. This is understandable as exporters are taking pre-cautionary measures ahead of China’s tighter food-safety measures which came into effect on 1 Jan 2013. Our view is that this is not a structural change in demand but a temporary hiccup as compliance can be achieved with better planning and marginally higher compliance costs.

[Maybank Investment Jan.2013]

- The tightness in supply of global 17 oils and fats with stock-to-usage ratio of 11.4% for the 2012/13F marketing year (2011/12: 12.3%) means that the world will rely on the ample palm oil stocks to satisfy global requirements.

- Furthermore, the near-historically wide discounts of CPO prices relative to soybean oil (3M futures on 31 Dec 2012: USD309/t) and rapeseed oil (USD423/t) makes CPO extremely attractive.

Graph below shows that stock pile in Malaysia build up heavily due to local refiners become uncompetitive against Indonesia's peers since Indonesia's export tax structure was revamped in 1.Oct.2011

- India and China are natural target market for CPO exports as India imposes a 7.5% import duty on refined palm oil but zero for CPO. Meanwhile, China imposes an import duty of 2% for CPO against 9% for edible oil. A boost of export will gradually reduce Malaysia's stock pile and boost CPO price.

- In July 2012, India reacted to Indonesia's tax reform by revising its benchmark import price for refined palm oil; effectively doubling import duty for refined palm oil to USD79/t (from USD36/t) back then. Fortunately, the Indian government has recently rejected a request by the Solvent Extractors Association of India to impose 10% import duty on CPO (currently tax free) and 20% on RBD palmolein (currently at 7.5%). The proposal to raise taxes was to help soybean farmers. Had the proposal been approved, this would have dampened demand for palm oil products in the near term. India is one of the world's largest consumers of palm oil at 6.6mil MT in 2010.

- China's Inspection and Quarantine Bureau has called for tougher quality measures on imported edible palm oil for the benefit of Chinese consumers come 1 Jan 2013. Palm oil shipments to China that do not meet the 2009 edible oils quality control specification on arrival at China ports (previously: shipped quality at origin) will be turned away. It seems "off-spec" shipment can no longer be re-fined at its shores. In essence, exporters/refiners are held responsible for the deterioration of oil quality during shipment. Officials from Malaysia Palm Oil Board (MPOB) was quoted as saying that approximately 95% of Malaysian edible oil exports to China meet China's stringent regulations (on arrival in China). The tougher measure imposed by China could slow down demand for refined palm oil in the short term given the uncertainties on its enforcement and as the industry adjusts to the new requirements.

- CPO price has traded at an average historical premium of USD208/t since 2006 over diesel price. Given the recent CPO price correction, CPO now trades near parity to diesel, a level not seen since end-2008. At this level, it is economically viable to produce and blend more palm biodiesel with fossil diesel wit little-to-no government subsidies.

- Europe Commission (EC) has approved the Roundtable on Sustainable Palm Oil (RSPO) scheme that would certify as sustainable transport fuel made from palm oil. This means palm biodiesel from sustainable sources qualify for subsidies and count towards the EU's renewable energy targets.

- In Oct 2012, the governors of eight states in the USA and almost 200 members of Congress asked the U.S Environment Protection Agency (EPA) to suspend rules that mandate production of ethanol for use in gasoline. EPA has since responded in Nov 2012 and turned down the request. A continuation of US biofuel mandate will ensure demand for bioethanol and biodiesel in the US to help sustain prices of corn and soybean, which has a positive carry on CPO price.

- The US Congress reintroduced the USD1 per gallon tax credit (RM860/t) for biodiesel as part of the comprehensive tax bill passed on 2.Jan.2013. The tax credit will be retroactively applied from 1.Jan.2012 and through the end of 2013. Recall that this biodiesel tax incentive was first introduced in 2005 which expired on 31.Dec.2011. With its reinstatement, the US National Biodiesel Board expects the tax incentive to promote expansion in biodiesel production in coming months, in line with the larger biodiesel admixture mandate of 1.28b gallons (or 4.5mil MT) in 2013. Note that soya oil covered 54%-55% of US biodiesel production in 2012. The reintroduction of this tax incentive will therefore boost US's import reliance of oils & fats in 2012/13 to satisfy domestic demand for food and non-food purposes.

- The plantation sector as implemented a RM650-RM850 per month minimum wage since 1.Sept.2011. On 1.May.2012, the Malaysian government announced a new minimum wage (effective 2013) at RM900 per month for Peninsular Malaysia and RM800 per month for East Malaysia. Minimum wage will have a marginal impact on the West Malaysia plantation players and a moderate impact on East Malaysian plantation players. Most if not all of the plantation workers are taking home more than RM1000 per month(inclusive of incentives and allowance) with some far exceeding the minimum wage.

- In end-Nov 2012, Indonesia's Ministry go Manpower also announced a minimum wage hike for 15(out of 33) provinces in Indonesia, ranging from a low of 8% to a high of 49%. Indonesia's minimum wage increase has averaged between 10-15% p.a. over the last few years. But hike for 2013 are phenomenal for some provinces especially East Kalimantan +49% YoY.

- This is a long term structural issue for Malaysian plantation estates in that Indonesia's rapid increase in minimum wages will continue to erode Malaysia's attractiveness as an employment destination for foreign workers. It is an open secret that plantation estates in Malaysia are already facing labour shortage (especially harvesters), and the industry is heavily reliant on foreign labour. Plantation estates in Malaysia will now find it even more difficult to retain and recruit Indonesian workers, especially estates in Sabah(as it borders East Kalimantan). This in turn will lead to an even higher wage bill for estates in Sabah over time.

[Maybank Investment Jan.2013]

- Malaysia's palm oil stockpile crept up to 2.63mil MT at end-deC 2012 (+2% MoM, +28% YoY), comprising record CPO stocks of 1.58mil MT (-6% MoM,+48% YoY) and processed palm oil stocks of 1.05mil MT(+17% MoM, +6% YoY).

- The marginally higher inventory is mainly due to better-than-expected CPO production of 1.78mil MT in Dec2012 (-6% MoM,+19% YoY) and weaker domestic consumption (-39% MoM,+151% YoY) whilst exports were largely flattish (-1% MoM,+4% YoY).

- Refinery utilisation rate improved to 76.4% in Dec2012 against an average of 62% for Jan-Sept2012.

[Maybank Investment Jan.2013]

- Palm oil is currently the cheapest edible oil in the market, enabling it to raise its market share. China, India and Pakistan are the three largest consumers of palm oil, taking up a combined 41% of global palm oil imports in 2011, based on statistics from the Oil World publication.

- CPO spot price has fallen 37% from its peak of RM3,568/tonne in 2012 to a low of RM2,231/tonne (as at 31 Dec 12) due to slower-than-expected demand which led to record palm oil stocks in Malaysia.

[CIMB Research Jan.2013]

- 印尼正修法限制新棕油公司的种植面积不得超过10万公顷,分析员认为,这会影响想要扩展业务至该国的种植公司(包括大马公司在内)。据报道,印尼正修订油棕种植相关法令,以限制新种植公司的种植面积在10万公顷。惟国有企业与合作社将可豁免,及新规定不会影响已拥有执照的种植公司。

http://www.nanyang.com.my/node/528470?tid=761 (April.2013)

2011年3月是油棕商业种植100周年纪念月,油棕最早种在印尼苏门答腊二个园丘里:浮罗拉惹(Pulau Raja)园及丹那依淡乌鲁(Tanah Itam Ulu)园,那是1911年的开荒年代。百年后的今天,棕油已被证明其永续性及社会经济存在的价值。

世界有17种油和脂,市场上(1790万吨),棕油(502万吨)+棕仁油(56万吨),产量居首(558万吨),占全球植物油的31%;大豆油(415万吨,23%)居次;动物油脂(251万吨,14%)及油菜籽油(237万吨,13%),排第3及第4位。

棕油近40年来随需求增加了10倍,原因是油棕产量高,价格比其他植物油便宜,占市场优势。

棕油+棕仁油生产国的总出口额合计为420.25万吨,等于全球植物油出口总额的61.5%。

主要进口国当然是中国、印度及欧盟,供不应求210.4万吨或55%

印尼和大马(占世界总产量85%)幸好有棕油幸好有棕油,为国家经济打拼,为扶贫助一臂之力。

专家说到2015年,世界需要棕油630万吨,在2011年的产量增加26%,到2020年再提升到770万吨,油棕种地必须扩张1200万公顷。

http://www.mpoc.org.my/Palm_Oil_Fact_Slides.aspx印尼和大马(占世界总产量85%)幸好有棕油幸好有棕油,为国家经济打拼,为扶贫助一臂之力。

专家说到2015年,世界需要棕油630万吨,在2011年的产量增加26%,到2020年再提升到770万吨,油棕种地必须扩张1200万公顷。

- Indonesia, the world’s biggest palm oil producer, will spend at least US$2.7 billion to build crude palm oil (CPO) processing facilities until 2014 to further boost the country’s CPO production capacity, an executive from the palm oil producer association has said.

- The new facilities will boost Indonesia’s processing capacity to 39.46 million tons a year in 2014, which will comprise 30.9 million tons for refining and fractionation capacity, 4.22 million tons for oleochemical production capacity and 4.34 million tons for biodiesel manufacturing capacity of 4.34 million tons.

- In the first quarter of this year, investors have spent around $1.02 billion on new processing facilities. The new investments are expected to increase the country’s total processing capacity to 30.9 million tons a year by year’s end, a 19.31 percent increase from the past year. The total processing capacities aimed for this year will consist of 25.1 million tons a year for refining and fractionation, up 24.88 percent from last year, about 2.2 million a year for oleochemical production and about 3.6 million tons a year for biodiesel manufacturing.

- Local industry players have said that the inflow of such sizeable investments was attributed to the government’s decision to change the export tax structure in late 2011, which effectively makes investments in the downstream industry more attractive. The new tax structure generates a margin of export tax on crude palm oil and downstream products, such as RBD palm olein of between 5.5 percent and 9.5 percent, making Indonesian products more competitive than those produced by Malaysian producers. Under the new tax regime, the export tax on processed palm oil products declines from 25 percent to 10 percent.

http://www.thejakartapost.com/news/2013/06/10/investors-spend-more-palm-oil-refineries.html (June.2013)

http://www.indexmundi.com/commodities/?commodity=palm-oil&months=60

http://www.palmoilhq.com/crude-palm-oil-cpo-futures/

- 提炼FFB = 得到 CPO & PK吗? 对。

- FFB的价钱,是根据 20% 的cpo 和 4% 的pk计算出来的,这个公式是自己发明的。如果要拿到这个价钱,必须是大公司。对于小园主来说, 要扣除暴利税, 东海岸价格更低, 厂商要求milling margin ,因此FFB收购价较低。http://bepi.mpob.gov.my/index.php/statistics/price/daily.html

http://www.investalks.com/forum/viewthread.php?tid=3544&highlight=tdm #15 tcs

- 四十年来,棕油在食油市场所占的份额,由5%到目前的超过40%,证明其优越性。在世界人口日增,各国日益富庶(食油消耗量与国民生产总值同步增长)及用途日广的趋势下,棕油前景亮丽。

http://www.nanyang.com/node/360888 (Year-2010)

- 最新的園丘行情,也反映出上述情況。數據顯示,樹齡9至18年的園丘平均價為每公頃4萬9千143令吉,平均產量是每公頃14公噸;至於樹齡4至9年的園丘,平均價格和產量分別是4萬5千920令吉和10公噸。

- 分析員指出,這些情況顯示,即使部份園丘的產量不高,只要地點適中,投資者依然願意出高價搶購,他們顯然不介意較低的短期回酬,而著重於長遠的利益。

http://biz.sinchew.com.my/node/55654 (Year-2011)

油棕种下后第三年就被列为“成熟”树,实际上还是没钱赚,要到第五年才略有盈利,这还要看原棕油的价格而定。

由第五年到第廿五年,盈利不断,但盛产期是由第七年至第十七年之间的十年,产量最高,如果原棕油价格挺秀的话,园主必然捞得盆满钵满,故园主对7-17最有好感。

由第十八年起,产量已开始走下坡;到第廿三年时已是树老叶黄,产量不多,到了要翻种的树龄。但是,如果原棕油价格奇高,像目前这样的话,园主也会拖延翻种,尽量利用其剩余价值,到第廿五年才翻种。

http://www.investalks.com/forum/viewthread.php?tid=3544&extra=&page=17 #330 wedals

CPO price

What affect CPO price?

- Supply & demand

- Stockpiles

- Raw materials (fertilizers) price

- Climate (e.g. La Nina)

- Prices of substitutes (e.g. soy oil)

1/2 year until 03-Dec-2012

半年内的油棕期货大约下跌了21%

1-year until 03-Dec-2012

从2011年4月的高峰期(8个月内)油棕期货大约下跌了36%

2-years until 03-Dec-2012

2年内的油棕期货大约下跌了42%

Video

Useful sites:

http://www.palmoil.tv

http://www.palmoilhq.com

http://bepi.mpob.gov.my

http://econ.mpob.gov.my

没有评论:

发表评论