2016年3月29日星期二

OWG控股(OWG,5260,主板貿服組)自從發紅股後,股價不升反跌,原因何在?

(1)大部份分析員都給該股極高的評價,事實是否如此?合理價是多少?

(2)檳城光大何時峻工?對該股能做出多大的貢獻?

(3)除了檳城的光大,是否尚有其他的企業活動來加強,以增加長期投資者的信心。

答:最近OWG控股是以5送1比例派發紅股,在2016年1月13日除權後,股價也相應地做出調整而往下調。過後,該公司股價則持續走低,相信是派發紅股利好消息被完全消化,即從之前的漲勢回調、或相信是股東認為是適當時機沽售套利所致。

先瞭解一點公司的業務性質;OWG控股為國內主題樂園業者,旗下業務擴展至飲食等其他業務。該公司旗下業務及資產包括Wet World系列主題水上樂園、娛樂休閒業、飲食業Only Mee等等。

該公司主要計劃為翻新檳城光大(Komtar Tower)。雲頂高原上的食閣、《全球大驚奇》(Ripley’s Believe it or Not)等,皆由該公司引進並管理。

(1)根據資料顯示,僅有極少部份的分析員有為該公司作出研究剖析,特別是聯昌研究做得較為積極及給予極高的評價。

事實是否如此,可看看該公司的最新業績及財務情況作為比較與參考。

截至2015年12月31日為止第二季,該公司的淨利為533萬4千令吉(每股淨利為2.88仙),前期淨利為415萬9千令吉(每股淨利為2.25仙)。第二季的營業額為2千834萬6千令吉,前期為2千456萬4千令吉。

總資產2億

首6個月的淨利為838萬6千令吉(每股淨利為4.53仙),前期淨利為720萬1千令吉(每股淨利為3.89仙)。該公司的每股資產值為80仙。

財務狀況方面,截至2015年12月31日,該公司的總資產為2億零839萬7千令吉,包括現金及現金余款為846萬令吉、在執照銀行存款為1千755萬8千令吉、其他應收款項/定存/預付款項為2千359萬8千令吉。

至於總負債為5千853萬4千令吉,包括長期借貸為4千零42萬1千令吉及短期借貸為257萬2千600令吉。

除了聯昌研究,沒有其他證券研究對該公司的近期剖析研究及推荐,所以沒有其他的目標合理價建議。

光大翻新4月1日峻工

(2)聯昌研究對該公司進行剖析及較為激進的推荐,而且都持著非常樂觀的態度。例如該行在去年杪的一份簡短的報告中,就認為一旦完成光大計劃重新開放後,該公司的股價可看高至8令吉。

根據聯昌研究的報告顯示,光大計劃將在2016年4月1日峻工開放。雖然該行都給予高價及極高評級,可是離市價還是有一段很大距離,顯示市場對有關評價,還是持著謹慎態度。

為雲頂進行主題樂園計劃

(3)根據資料顯示,該公司在完成翻新光大工程後,也為在雲頂進行20世紀霍士主題樂園計劃,後者預料會在2017年才完成。去年杪,據悉該公司有接獲一些併購建議,惟至今尚沒有進一步的詳情與進展,可注意該公司日後是否有類似的的宣佈。(

Bulls making a comeback

Foreign funds are putting money in emerging markets

HUMAN beings have a natural tendency to fear heights – it’s a natural survival instinct which worked well in the wilderness and in the outback, but one which severely plays against us when it comes to the stock market.

Seven years ago, back in early 2009, these were some of the top financial headlines in the US:

> George Soros says US banks ‘basically insolvent’

No one knew it then, but the Dow Jones was about to embark on a seven-year bull run and would gain some 92% over that period. Riding along was the FBM KLCI, which gained 85% over the same period.

For sure the ride has been bumpy and riddled with sharp corrections. But for investors who held on to their stocks, they would have been rewarded with handsome returns.

For any investor invested in the market – volatility will always be there. But as long as they are able to endure the frailty and fluctuations of the market, the long-term rewards historically outweigh the short-term fickleness.

We have heard it many times before – the best time to own stocks is when sentiment is at its worst,

This was especially apparent in early 2009 when the US economy was on the brink of a banking collapse, In those dark days, there were more forecasts of Black Mondays than predictions of light at the end of the tunnel.

Eng: ‘The market has had a good run since January.’

The stock market, as always, had a mind of its own. Despite the proclaimation of dooms and the fall of many American banks, the Dow was heading almost on a straight upward trajectory by mid-March 2009.

Sir John Templeton said: “Bull markets are born on pessimism, grow on skepticism, mature on optimism and die on euphoria.”

That was true seven years ago, 50 years ago, and definitely just as true today.

Logically speaking, what comes down must go up.

Earnings can still be nasty, but doesn’t the market always behave a year forward. At the heart of it all, the market is made up of buyers and sellers. All it takes are a few buyers during a down period to sniff out an opportunity, and suddenly, the market is edging upwards.

It’s the same story with oil prices. Do not expect the coast to be completely clear – for example no more excess inventories, oil demand significantly outpacing supply or the Organisation of the Petroleum Exporting Countries (Opec) deciding to cut production by 50% – before we see oil prices moving up.

By the time these signs are crystal clear, oil prices have made new highs months ago.

In any case, last week the International Energy Agency (IEA) said that oil prices had bottomed out due to US and other output cuts outside the Middle East-dominated Opec.

The US rig count fell for a 12th straight week last week to a total of 386, its lowest since December 2009 as drillers continue to slash capital expenditure.

Zulkifli: ‘These are still early days of a recovery. People are still sceptical ...’

The problem now is that after a seven-year run, investors are getting nervous. Investors have mostly been in a flux wondering where the market is heading. Most investors are waiting for the crash to come. They talk about a sluggish economic outlook, falling earnings, recessions in commodity-heavy nations, slowing growth in China, negative interest rates, the end of quantitative easing in the US, the UK (potential Brexit) and flatter yield curves.

Has the market stalled and lost some of its stamina? With the expectation only of mediocre growth and low yields, is it time to sell stocks?

Behind the scenes, some under-appreciated indicators are starting to show some light.

First of all, the ringgit has been strengthening – a reflection of foreign money coming back to Malaysia. It strengthened 0.6% this week to RM4.09 against the greenback.

Last week, foreigners bought listed equities amounting to RM1.04bil on Bursa Malaysia, higher than the RM972.2mil acquired in the preceding week. To date, there are some 12 consecutive weeks of total net inflows and brings cumulative year-to-date foreign purchases to RM1.6bil.

For the entire 2015, there was a net outflow of RM19.5bil.

Meanwhile the FBM KLCI closed at 1,703.19 on Thursday, which is also its six-month month high. The seven-month high is 1,744.19 recorded on Aug 3, 2015.

From a charting perspective, a recovery in the FBM KLCI appears to be playing out.

“We reiterate our view that KLCI must close above 1700 levels convincingly to sustain the ongoing rally from 1600, with key upside target at 1710 (March 7 high), 1727 (Oct 19 high) and 1740 (200-day simple moving average) levels. Failure to close above 1700 will see the index continue its short-term congested range-bound consolidation within the 1660-1700 territory,” says Hong Leong analyst Nick Foo.

Etiqa Insurance & Takaful head of research Chris Eng, on the other hand, feels that the market is toppish for now.

“The market has had a good run since January. It may have a few more legs to run, but come April, it will be earnings results in the US, and in May, it will be earnings result in Malaysia. We aren’t expecting very positive earnings coming out, so market may start falling again by April,” says Eng.

From a trading perspective, he would ask clients to sell into strength.

On a fundamental perspective, however, he isn’t expecting a recession, well at least not this year. He would still advice investors to stay invested in equities.

“We are expecting some weakness in the market come middle of the year. That would be a better time to buy. We would identify that weakness and look for opportunities then,” says Eng.

MIDF Research has been recommending its clients to start buying since the start of the fourth quarter last year.

“These are still early days of a recovery. People are still sceptical, especially retail investors. But we have been tracking the money flows, and foreigners have been net buyers every single day of the 14 trading days so far this month, which is a phenomenon not seen in more than two years” said Zulkifli Hamzah, head of MIDF Research.

According to Zulkifli, the Malaysian equity market is benefiting from a tide of global liquidity flowing into Asia. Some of the money is actually global funds in China, being reallocated to other Asian markets as the outlook in Asia’s biggest economy is challenging.

“In the bond market, Malaysia started to look attractive to the foreigners as early as September last year. The low global interest rate environment, with negative rates in some countries, has made local yields very attractive indeed. That is reinforced by the depressed Ringgit,” said Zulkifli.

“Overall, we are positive on the market. Sceptism of the market has been partly due to the relatively restrained climb in the index. But this has been due to selling by local funds, which are understandably taking the opportunity of the market’s upward march to realize their profits. We also do not expect to see such a steep incline in the indices because of rotational forces at work,”

“Global investors are not going to come in and buy blindly across the board although the Ringgit is seen as undervalued. They will be selective and buy only those stocks that they see value. We believe the current uptrend has legs. However, there are potential potholes which may cause temporary retracement, at which point it would be opportune to enter the market,” said Zulkifli.

He added that the changing of guard in Bank Negara and the Sarawak state election would be closely watched by foreigners.

No rate hike is good for Malaysia

On Wednesday, Federal Reserve officials lowered their view of the economy and said they likely won’t raise interest rates as swiftly as they had previously anticipated as there are lingering risks posed by soft global growth and financial-market volatility.

Policy makers left short-term interest rates steady and said they would raise their benchmark rate just twice this year, after an initial increase in December 2015, down from the four they previously predicted.

Last week European Central Bank (ECB) chief Mario Draghi announced a much bigger and wider-ranging stimulus package than anyone had expected

He increased his purchases of financial assets by a hefty 20 billion euros per month (from 60 billion-80 billion euros), pushed interest rates lower into negative territory (by 10 basis points), improved financing for the banks and announced his intention to buy investment grade corporate bonds.

In other words, the ECB will pay banks 0.4% to lend. This puts the eurozone in a negative interest-rate situation.

This move inevitably makes Malaysia more attractive.

Recessionary pressures and low interest rates in the US are a boon for emerging markets like Malaysia. This is further helped by economies like Japan and China which are continuing to cut interest rates to kickstart their economies.

With US and eurozone interest rates having stayed in negative territory for so long, and doubts on future rate hikes, investors are getting desperate for yields.

So they come to Malaysia, where the average yield on a 10-year dollar bond is higher by some 140 basis points than a similar US Treasury 10-year note.

Also, after a torrent of bad news, some confidence is returning to Malaysia.

Last month, Fitch Ratings affirmed Malaysia’s long-term foreign and local-currency issuer default ratings (IDRs) at A- and A respectively, with stable outlook.

Malaysia’s senior unsecured local-currency bonds were also affirmed at A while the country ceiling was affirmed at A and the short-term foreign-currency IDR at F2.

The three rating agencies – Moodys, S&P and Fitch Ratings – have given the same credit rating of between A3 and A- with stable outlook for Malaysia.

Bank Negara also announced that Malaysia’s economy grew by 4.5% in the final quarter of last year, which was better than expected. This brings the full-year gross domestic product growth to 5% from 6% in 2014.

The recent stability in the ringgit was also a positive factor for foreign investors, and this has taken away some of the foreign exchange risk of investing here.

The ringgit is the best-performing emerging-market Asian currency over the past three months, having been one of the worst performers last year. Year-to-date, the ringgit has gained 2.05% against the US dollar.

The economy is on a better footing now that the Government has revised its budget based on oil prices between US$30 and US$35, and the country is on track to achieve its targeted budget deficit of 3.1%.

Low PE Low PTBV Dividend Yield Stocks

Price EPS DPS NTA PE DY ROE PTBV Mcap(M) DPO Name Code

0.34 4.32 1.98 0.57 7.87 5.83 7.34 0.58 371.28 0.46 L&G 3174

1.10 11.09 4.03 2.46 9.92 3.67 4.47 0.44 548.90 0.36 LTKM 5843

0.48 5.96 1.99 0.76 7.97 4.20 7.84 0.62 147.25 0.33 PANTECH 5232

0.38 4.27 2.01 0.84 8.89 5.29 5.09 0.45 142.73 0.47 HUAYANG 9962

0.59 6.27 2.54 0.79 9.42 4.31 7.64 0.72 360.91 0.41 TROP 5125

0.93 12.08 5.00 1.02 7.70 5.37 11.84 0.91 73.09 0.41 GLOMAC 7227

1.11 11.48 3.75 2.28 9.67 3.38 5.04 0.49 367.42 0.33 PMBTECH 5041

1.60 26.09 11.05 1.65 6.13 6.91 15.78 0.97 676.60 0.42 PENSONI 5110

0.84 12.08 4.21 1.35 6.91 5.04 8.88 0.61 604.94 0.35 AMBANK 5020

1.18 13.21 4.66 1.16 8.93 3.95 9.50 0.85 194.75 0.35 ASTINO 7169

1.56 16.03 7.50 2.11 9.73 4.81 7.60 0.74 658.73 0.47 UOAREIT 1724

0.92 11.98 4.01 1.08 7.68 4.35 11.12 0.85 147.12 0.33 YOCB 5159

1.29 15.94 8.00 1.70 8.09 6.20 9.38 0.76 414.02 0.50 ORIENT 5133

1.83 18.32 8.48 2.69 9.99 4.64 6.79 0.68 506.84 0.46 PENERGY 6491

0.98 9.97 4.00 1.86 9.78 4.10 5.36 0.52 75.54 0.40 PARAMON 7172

0.34 4.32 1.98 0.57 7.87 5.83 7.34 0.58 371.28 0.46 L&G 3174

1.10 11.09 4.03 2.46 9.92 3.67 4.47 0.44 548.90 0.36 LTKM 5843

0.48 5.96 1.99 0.76 7.97 4.20 7.84 0.62 147.25 0.33 PANTECH 5232

0.38 4.27 2.01 0.84 8.89 5.29 5.09 0.45 142.73 0.47 HUAYANG 9962

0.59 6.27 2.54 0.79 9.42 4.31 7.64 0.72 360.91 0.41 TROP 5125

0.93 12.08 5.00 1.02 7.70 5.37 11.84 0.91 73.09 0.41 GLOMAC 7227

1.11 11.48 3.75 2.28 9.67 3.38 5.04 0.49 367.42 0.33 PMBTECH 5041

1.60 26.09 11.05 1.65 6.13 6.91 15.78 0.97 676.60 0.42 PENSONI 5110

0.84 12.08 4.21 1.35 6.91 5.04 8.88 0.61 604.94 0.35 AMBANK 5020

1.18 13.21 4.66 1.16 8.93 3.95 9.50 0.85 194.75 0.35 ASTINO 7169

1.56 16.03 7.50 2.11 9.73 4.81 7.60 0.74 658.73 0.47 UOAREIT 1724

0.92 11.98 4.01 1.08 7.68 4.35 11.12 0.85 147.12 0.33 YOCB 5159

1.29 15.94 8.00 1.70 8.09 6.20 9.38 0.76 414.02 0.50 ORIENT 5133

1.83 18.32 8.48 2.69 9.99 4.64 6.79 0.68 506.84 0.46 PENERGY 6491

0.98 9.97 4.00 1.86 9.78 4.10 5.36 0.52 75.54 0.40 PARAMON 7172

Increase holdings in AirAsia.

27 November 2013

AirAsia has always been one of my favourite company.

Besides all those negative factors that affect its short-term prospect,

I had never doubted about its long-term profitability and growth potential.

Hence, I see the recent price correction of its share as an opportunity to increase my holdings, and just bought 2000 shares of AirAsia at RM2.40.

Now the company forms ~10% weight in my portfolio.

Besides all those negative factors that affect its short-term prospect,

I had never doubted about its long-term profitability and growth potential.

Hence, I see the recent price correction of its share as an opportunity to increase my holdings, and just bought 2000 shares of AirAsia at RM2.40.

Now the company forms ~10% weight in my portfolio.

05 November 2012

Increase my investment in AirAsia.

Pump in new fund, bought 3000 shares of AirAsia...

now the investment in AirAsia had contribute ~20% weight in my portfolio.

I'm quite optimistic about the growth potential of AirAsia. Its operation in Malaysia would probably continue to grow at rate of 5~10%p.a. though the LCC market already quite matured. The growth momentum of AirAsia would mainly come from its aggressive expansions into regional markets, i.e. Thailand, Indonesia, Philippines, Japan... Taking these into account, I believe that AirAsia's profit in the coming years will grow at a rate of 15%p.a. or higher .

.

17 June 2009

AirAsia 2008 - Operational Cashflow still Strong.

Due to its weak performance in 2008, the shareholders of AirAsia had been worried about its gearing and coverage ratios.

This article is just a simple analysis on AirAsia's 2008 cashflow, which is an important measure of the company's ability in servicing its debts.

According to its audited account, AirAsia's cashflow from operation in 2008 is negative RM 416 million. This number, however, is what we get after charging the unwinding loss on derivatives. Seeing that the huge cash outflow of this unwinding process is not neccesarily to be recurring, we should exclude them from our analysis so that we can get a more accurate picture on AirAsia's real performance.

How much cash had AirAsia actually paid in the unwinding transactions? According to its report, the total unwinding loss incurred is RM 1.1 billion. The loss is allocated and borne by three entities of AirAsia:

- AirAsia Malaysia: RM 679 milion

- Thai AirAsia: RM 222 million

- Indonesia AirAsia: RM 207 million.

Thus, instead of RM 679 milion, the total amount of RM 1.1 billion should be used for our adjustment on AirAsia's cashflow. After the first adjustment, the operational cashflow of AirAsia had become a positive RM 691 million.

Thus, instead of RM 679 milion, the total amount of RM 1.1 billion should be used for our adjustment on AirAsia's cashflow. After the first adjustment, the operational cashflow of AirAsia had become a positive RM 691 million.Then, due to the reason discussed in my previous post (regarding the recurring nature of the fuel-hedging transactions), I'll charge back a cash outflow of RM136 million (equal to 20% of RM679 million) into AirAsia's cashflow account. After this second adjustment, AirAsia's operational cashflow of 2008 would be a positive RM 555 million.

Compared to the company's cash outflow on interest (RM 240 milion) and repayment of borrowing (RM 301 million), the operational cashflow can be considered as strong, and its cashflow ratios is within my comfort zone.* This figure is from the perspective of AirAsia company only. Because I can't get the information on the cashflows of TAA and IAA, analysis from the level of whole AirAsia Group can't be done.

However, this cashflow performance is still below my initial expection. In 2009, I hope that AirAsia can make a huge improvement, generating an operational cashflow of no less than RM 1 billion.

16 June 2009

Dissecting AirAsia's Earning 2008 (Part2)

Here, we examine AirAsia's financial performance, taking into account the profit/loss from Thailand AirAsia (TAA) and Indonesia AirAsia (IAA).

Revenues of the jointly-control-entity & associates in 2008:

- TAA: RM 889 million

- IAA: RM 482 million*

- TAA: RM -118 million

- IAA: RM -83 million*

The net losses stated above are after the adjustment discussed in part-1, i.e. I took out the whole unwinding loss on derivatives (RM 222 million for TAA, RM 207 million for IAA), and then charge back 20% of its amount .* Besides IAA, AirAsia has a number of other associates. In the sense that their contribution should be quite small, I assumed that the figures of revenue/loss from associates as reported in AirAsia's statment are all derived from IAA.

The above losses are not reflected in AirAsia's reported income statement, because the associate's results are consolidated into AirAsia's statement using equity method, and their equity had become zero since few years ago. However, to gauge the economic performance of AirAsia as a grouop, these unregconized losses should be taken into account.

Consolidating the share of loss (48.9%) from these associates, AirAsia's results in 2008 will turn negative -- a net loss of RM 38 million. It should be pointed out that the shared profit/loss from the long-haul AirAsia X had not been included here. However, its contribution in 2008 should be quite small and hence negligible.

Next, we examine AirAsia's performance from the perspective of whole AirAsia Group. Here, we consolidate 100% of TAA & IAA's revenue and results with AirAsia Malaysia. In my opinion, this is the most appropriate measure of AirAsia Group's performance. (see the reasons here.)

Next, we examine AirAsia's performance from the perspective of whole AirAsia Group. Here, we consolidate 100% of TAA & IAA's revenue and results with AirAsia Malaysia. In my opinion, this is the most appropriate measure of AirAsia Group's performance. (see the reasons here.)The figures after consolidation are:

- Revenue: RM 4.00 billion

- Profit/loss: RM -141 million

- Profit margin: -3.5%

15 June 2009

Dissecting AirAsia's Earnings 2008 (Part 1)

As pointed out in my older posts, AirAsia's reported earnings need some adjustment before the numbers can be used to gauge its performance.

To dissect AirAsia's 2008 earnings, let's begin with the reported numbers in its Income Statement:

- Profit before tax (PBT) : RM -869 million

- Profit after tax( PAT) : RM -497 million

- Earning per share: -21.1 sen

- unwinding derivatives (interest-rate swaps): RM -152 million

- unwinding derivatives (fuel hedging contract): RM -678 million

- foreign exchange movement on borrowings: RM -235 miilion

But I would like to discuss further about the validity of the adjustments done. Those 3 items are excluded because they are thought to be non-recurring in nature. But are they really so?

In my opinion, the FX movement is quite volatile and the trend is difficult to predict, thus its short-term movement can be considered as non-recurring. But fuel-hedging is a different case. Every airlines in the world will more or less hedge their fuel consumption. AirAsia's current position without any hedge is just a short term bet on the movement of oil prices. Sooner or later, it will resume oil-hedging activities.

So, the unwinding decission taken by AirAsia last year, is like charging all the future loss into one year. This action will make its 2008 earning worse, at the same time inflate its future reported income (less loss from hedging).

I suggest that we charge a portion of the unwinding loss back into AirAsia's income.

According to its quarterly report (Sep-2008), the original intention of AirAsia when entering these contracts is to hedge its fuel cost in the remaining period of 2008 and year 2009. Lacking of any detail information, I think the unwinding loss of these contracts (RM 678million) should be spread evenly over the five quarters starting Q4-2008. As a result, a loss of RM136million (= 20% x RM678million) should be charged into each of these quarters to bring down the inflated earning.

As a result, AirAsia's adjusted earning in 2008 will become RM 60 million, or 2.5 sen per share.

.

03 November 2008

Profit of AirAsia (Part 2)

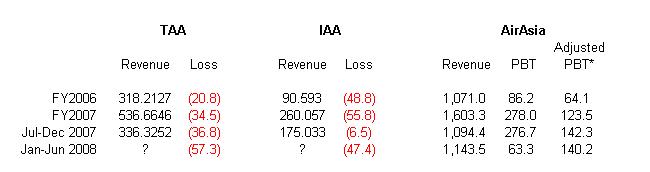

The main purpose of this article is to discuss why we should examine the economic performance of AirAsia from the perspective of the whole AirAsia Group, i.e. we should consolidate the statements of AirAsia with 100% revenues and profit/losses from TAA & IAA.

First, let’s have a look at the revenues and profit/losses of the three entities in AirAsia Group, presented separately in the following table (all figures are RM illion):

- (the Jan-Jun 2008 revenues for IAA & TAA are not announced yet.)

- * Adjusted PBT of AirAsia shown excludes non-operating items, but not including the profit/losses from IAA & TAA.

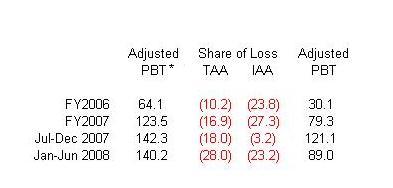

If we include the share of losses (48.9%) from TAA & IAA into AirAsia’s income, then AirAsia’s profit will be as shown in the following table (as discussed in my previous post):

After these adjustments, the earnings of AirAsia will be about 8.9 sen per share (twelve months ended Jun-2008). If we accept this figure, then the current PE ratio of AirAsia is just around 12x, which is a very attractive level for me due to the high potential of AirAsia's earning growth in the coming years.

However, I still think the above adjusted figure is not reflecting the real economic performance of AirAsia. In my opinion, these figures may have been distorted by two factors – the asset allocation in AirAsia Group, and the transactions between the entities in the Group.

Let’s discuss them one by one.

.

1. the asset (aircraft) allocation of AirAsia.

As we know, currently there are two types of aircrafts in AirAsia Group – the old Boeing-737, and the brand new Airbus-320. And we know that the later is the more profitable one due to its oil-efficiency and low maintenance cost. So, the routes served by Airbuses are more profitable than those by Boeing, especially in recent periods of high oil price.

What happening in AirAsia Group is, the allocation of Aircrafts is not even among the entities in the Group. AirAsia Malaysia is operating almost all the Airbuses, while the old Boeings are being pushed to TAA and IAA.

For example, according to the figures announced for the quarter ended Jun-2008, out of the 39 airbuses in the Group:

- 35 of them are allocated to AirAsia Malaysia,

- only five are in TAA,

- and none in IAA.

In other words, AirAsia pushed the non-profitable assets to its associates, and retained the most profitable assets within Malaysia. This might be one of the reasons why TAA and IAA are suffering continuous losses while AirAsia is making great profit.

So, if we adjust AirAsia’s income statement using only 48.9% share of losses from TAA and IAA, we are giving more weight on the Airbuses, and have a lower weights on the poor-performing Boeings. As a result, we will get an upward-biased figure about the Group’s performance.

Some people may argue that AirAsia Group is replacing all the Boeings with Airbuses. Thus TAA and IAA might become as profitable as AirAsia (Malaysia) after the replacement. So, the upward biased figures of AirAsia’s statements is a more accurate measure of Group’s future performance (After all, the future performance should be most concern to the shareholders, right?)

I will not agree to this argument. Though AirAsia is accelerating the retirement plan of the Boeings, it will take several years to complete the plan. By then, the new Airbuses today may become aged, and their maintenance will become higher, and who knows, they may just become like the old Boeings today. So, to be consecutives, I think we’d better use today combination of assets (a mix of new and old) even when we are estimating the Group’s future performance.

.

2. The transaction between TAA, IAA and AirAsia. (the Aircraft Rentals)

As we know, all the aircrafts of the Group are owned by AirAsia. So, to operate those aircrafts, TAA and IAA have to pay rental fees to AirAsia. This is another part that may distort the reported performance of AirAsia.

When AirAsia receive rentals from TAA & IAA, it’s recorded as an income, which is off course 100% reflect on AirAsia’s earnings. So, the higher the rental, the more it benefits AirAsia. But from the view of TAA or IAA, these rentals are expenses. That means a higher rental fees will reduce their profit (or increase their losses), i.e. a higher fee will have a negative impact on them and thus AirAsia.

Again, because AirAsia owns 48.9% stake in TAA and IAA, only half of the rental expenses in TAA and IAA would be consolidated into AirAsia’s statement, while 100% of AirAsia’s rental income will be reflected on the same statement. So, by simply charging a higher rental fee, AirAsia could increase its reported earnings without improving its operating performance.

From the perspective of the whole AirAsia Group, the rental fee among entities shouldn’t have any effect on the overall performance. So, we should consolidate 100% of the revenues and profit/losses of TAA & IAA into AirAsia’s statement, to get a clear picture on the Group’s operating performance.

.

Conclusion:

By treating three entities as a group, we can eliminate the potential distortion of AirAsia’s economic performance from both its asset allocation policy and the aircraft rental fees.

The following table shows the 100% consolidated revenue and profit/losses for AirAsia Group. Profit margins of AirAsia (Malaysia only) are included in the table for comparison purpose. (Revenues and PBT are in RM million, Margins are in %).

- The 3rd column (AirAsia Margin) is calculated using PBT reported in AirAsia’s statement.

- The 4th column, Adjusted AirAsia Margin, are reported figures excluding non-operating items (the foreign exchange gain and selling of interest rate swap contracts), and not including profit/losses from TAA and IAA.

- the Group’s PBT and Margin are also excluding non-operating items.

.

29 October 2008

Profit of AirAsia (part 1)

This article is some discussion about AirAsia's reported profit. By pointing out some accounting pitfall in its statements, I hope that this article can present a more accurate picture about the profitability of AirAsia.

Before we start, let's have a glance on the profit reported by AirAsia in recent years:

- FY 2006 (ended June-2006): RM 86.2 million

- FY 2007 (ended June-2007): RM 278.0 million

- 6-month ended December-2007: RM 276.7 million

- 6-month ended June-2008: RM 63.3 million

All the figure above are PBT (profit before tax). I think PBT is a more accurate measure of AirAsia's profit because its after-tax-profit figures are highly distorted by the "deferred tax" item. (For more about this, please read: My Mistake - the "Defered Tax" in AirAsia's profit )

Nevertheless, there are two things we had to be cautious about these PBT figures.

.

1. Special Income.

First, we should adjust the profit against non-operating income. A significant item in AirAsia's statements is the "foreign exchange gain". As we know, AirAsia has huge amount of loans that is denominated in USD. As a result of USD depreciation in recent years, AirAsia had recorded some "foreign exchange gain". However, most of these "profits" are just accounting gain, which won't generate any real cash flow or economic value.

This is because AirAsia had entered into some foreign exchange forward contracts, which help it to hedge against the appreciation of USD (these contracts had swap the future repayments of AirAsia's loan from USD into Ringgit). So when USD depreciates and the loan amount of AirAsia is decreased, AirAsia should suffer a comparable amount of loss in the value of its hedging contracts. The problem in AirAsia's income statement is, it only regconized the exchange gain from the decreased amount of loan, and doesn't take into account the loss of its foreign exchange contracts (they are "off-balance sheet item" and not reflected on income statement).

Due to some reasons, (e.g. AirAsia is not doing 100% hedge on its loan amount, the fair values of forward contracts also affected by market activities, etc.), the actual gain/loss from foreign exchange rates are more complicated. However, it's quite sure that the real total gain/loss is much smaller than the figures reported in AirAsia's income statement. So, to be conservative, we'd better exclude all the foreign exchange gain/loss to get a clearer picture on AirAsia's profitability.

Besides the foreign exchange gain, AirAsia had also recorded a gain from selling someinterest-rate swap contracts during FY2007.

The adjusted profit of AirAsia, excluding those special items, are summarized as follow : (all numbers are RM million)

.

2. The Losses in Thai AirAsia (TAA) and Indonesia AirAsia (IAA).

Until today, TAA and IAA still suffering loss.

AirAsia owns 48.9% stake in TAA and IAA. Thus the same portion of losses from these two entities should be reflected on the income statement of AirAsia. However, AirAsia had stop recognizing these losses from both TAA and IAA.

Again, it's because of the accounting method used.

AirAsia's investments in TAA and IAA are accounted for in its consolidated financial statements using equity method of accounting. The following paragraph is extracted from AirAsia's annual reports:

- The Group discontinued recognition of its share of further losses made by Thai AirAsia as the Groups interest in the jointly controlled entity has been reduced to zero and the Group has not incurred any obligations or guaranteed any obligations in respect of the jointly controlled entity.

The reason is simple. First, TAA, IAA and AirAsia are operating as a group (e.g. they share the same ticket booking system), thus they should be considered as parts of a whole body. Second, AirAsia is leasing its aircrafts to TAA and IAA, so they have to pay rental fee and maintenance charge to AirAsia. If their operation continue to face difficulties, it's possible that they will postpone the payments or, worse, fail to meet their payment obligation. Thus, the fact that TAA & IAA are "limited company" doesn't stop AirAsia from bearing the risk of their further losses.

The following tables list the related parties transactions between AirAsia and TAA & IAA, a simple illustration about their relationship.

1. AirAsia's income (RM million) from TAA and IAA:

2. Amount of money that TAA & IAA owe AirAsia (RM million):

.

Conclusion:

To have a fair evaluation on AirAsia's profitability, the non-operating gain/loss should be excluded, and the profi/loss from TAA & IAA should be included. Thus, the real profit of AirAsia in the past few years should be as follow:

(* the first column is the adjusted profit excluding non-operating item).

As we can see, these figures are much smaller than the PBT reported in AirAsia's income statment.

.

...... continue reading : Profit of AirAsia (part 2)

.15 June 2008

Why I'd never worried about AirAsia's debt.

One of the reasons that investors don't like AirAsia is the huge amount of CAPEX and borrowings.

In this article, I'll discuss how good is AirAsia in managing its debts.

1. Interest rate hedge

Interest rate hike is a essential risk for highly debted company. AirAsia hedges against the risk by entering into interest rate swap contract that will convert almost all of its debt into fixed rate debt.

According to its Dec-2007 report, AirAsia’s swap contract obliges it to pay fixed interest rate of between 4.78% and 4.90% instead of being subjected to the floating US-LIBOR for the entire loan amount over the entire tenor.

The hedging of interest rate will stabilize AirAsia' future cash flow, and help it to maintain the current low interest rate throughout the whole repayment period.

2. Forward foreign exchange hedge

As the borrowings of AirAsia are all in USD, it will benefit from the depreciation of USD. Moreover, Airasia had entered into forward exchange contracts for settlement at fixed Ringgit rates when the USD had depreciated.

For example, as disclosed in Dec-2007 report, AirAsia had swap its RM3.3 billion equivalent debt into ringgit at exchange rates between RM 3.000 ~ RM 3.369. Because the exchange rate of USD to Ringgit is much higher when it borrowed the money, AirAsia is actually making a profit from the repayments of principal loan amount.

These profits from foreign exchange had been recorded in AirAsia’s income statement. In the latest quarterly reports, we can see that the financial cost of AirAsia is a positive value (which means it’s an income, not expenses). This is because the foreign exchange gain from the repayment of debt is higher than the interest expenses.

The following table shows AirAsia’s interest expenses & foreign exchange gain during pass two years.

And the most important part is, these exchange profit are recurring! (because AirAsia had swapped its debt into ringgit at a favorable rate.) With this recurring income, I never doubt the ability of AirAsia to pay the interest of its loan.

3. Tax Incentive

AirAsia has been granted a great amount of tax incentive from our government, for its CAPEX in purchasing aircrafts.

How much is the tax incentive? Let’s look at the recent figures.

From my own estimation, for every dollar AirAsia spent in purchasing aircrafts, the tax incentive incurred is enough for it to pay the loan interest for at least 3 years! As the repayment period of AirAsia’s loans are only 12 years, the tax-incentives had actually helped to cover a substantial part of its financial cost.

So, why not borrowing?

Let’s look at this tax incentive from another angle of view. The following table shows the PBT of AirAsia and the tax it should have paid if there’s no incentive:

And the actual taxes paid by AirAsia during this period are:

- FY2006:RM 2.2 million.

- FY2007:RM 5.1 million

- July-Dec 2007:RM 1.5 million

In fact, the fast expansion of AirAsia, leveraging on financing facilities, is one of the factors that enable AirAsia to maintain its profitability. Because in the highly competitive LCC industry, only the lowest cost player (through effective cost reduction, economic scale, and fast penetration into the market) will survive and prosper.

Since it's able to manage its debts so well, I think AirAsia's way of expansion (through borrowings instead of issuing new shares) is the best way to benefit the shareholders without diluting our interest in the company.

.

[updated 29-10-2008]: There's a serious mistake in this article -- the foreign exchange gain reported in AirAsia's income statement is not a real gain. Though I don't know the exact figure, I'm quite confident that AirAsia's actual (recurring) exchange gain/losses should be much smaller than the figures stated in this article. For more detail, pls read my post: Profit of AirAsia (part 1).

.

03 February 2008

AirAsia: the McDonald’s in aviation industry?

Few days ago, I found that AirAsia’s business model is somewhat similar to McDonald’s -- It is going to generate a huge income from the leasing of aircrafts.

The story of my discovery started from last year, when I realised that I had made a serious mistake in analysing AirAsia -- I ignored the deferred tax item in its financial statement. Since then, I had gone through AirAsia’s financial report again, again, and again, just to make sure that there’s nothing else that I’ve missed.

Then, I discovered an interesting item in the reports —- the aircrafts.

First, let’s introduce two entities that's related to AirAsia -- Thai AirAsia (TAA) and Indonesia AirAsia (IAA). Some people may think that TAA and IAA are subsidiaries of AirAsia. But, in fact, they are not wholly owned by AirAsia. TAA is only a jointly controlled entity of AirAsia, and IAA is an associate company. Both of them started their operation in 2004, and AirAsia only owns 49% stake in each of them. AirAsia had paid USD 5.26 million (about RM 20 million) to get the 49% share of TAA, while IAA’s only cost AirAsia USD 2.00 (two dollars).

Since beginning of their operation, TAA and IAA never own an aircraft. All the aircrafts in operation are either owned by AirAsia, or leased by AirAsia from other parties. AirAsia then lease or sublease these aircrafts to TAA and IAA. They would then, of course, pay a rental fee to AirAsia.

The table below show how much money AirAsia had collected each year, from the leasing of Boeing aircrafts to TAA and IAA. I have included the PBT and Net Cash from Operationof AirAsia in this table, for comparison purpose.

As we can see, the income from leasing aircrafts is quite significant when compared to AirAsia’s PBT, or operational cash.

As we can see, the income from leasing aircrafts is quite significant when compared to AirAsia’s PBT, or operational cash.However, the actual earning from these leasing activities should be quite small, because most of these aircrafts are not owned by AirAsia. (The company only owns six Boeing aircrafts). AirAsia lease the Boeings from other party and sublease them to TAA or IAA. I don’t think AirAsia can make a good profit out of this.

But in the next few years, AirAsia’s fleet size will grow dramatically. Due to the latest information, it has 175 confirmed order of Airbus. According to the current planning of AirAsia's management, more that half of these aircrafts will be leased to TAA or IAA. Then, the rental income may have a great contribution to AirAisa's profit.

This is similar to what McDonald’s did about 50 years ago. In the early stage of its expansion, McDonald’s signed long-term lease-contracts with some property owners to rent their properties, and then subleased those properties to its franchisees. Later, while McDonald realized the great potential of rental income, it started to buy its own properties. Then, the rental income had gradually become the most important part of its profit.

So, while AirAsia's fleet size is expanding, will the rental income (of aircraft) gradually play an important role in AirAsia's profit?

Well, maybe it's too early to make a conclusion now. Let's wait and see......

.

10 December 2007

My Mistake - the "Defered Tax" in AirAsia's profit

In AirAsia's financial statement, There's a very important item, named "deferred tax". I didn't have any idea about what is it and what it means. (because I was a science-stream student, and never learn about accounting in school). I thought that it's some kind of complex taxing calculation, and I'd just ignored it in my previous analysis of AirAsia.

But, later I found that this "deferred tax" play an important role in AirAsia's financial statement. It made up about 20% of AirAsia's equity, and more than 40% of AirAsia's PAT! So, I think it's a MUST to understand what is it, and where it comes from.

After some readings and studies, I've get some idea about this "deferred tax". I understand that, due to the International Accounting Standard, this "deferred tax" is allowed to be recorded in an income statement. But I really doubt that this is a proper practice in reflecting the financial performance of a company.

The "deferred tax" item in AirAsia, for example, represent the tax credit given to the company. Though this tax credit is incurred during current year due to the company'sCAPEX, it can only be realised/utilised in the future, i.e. when AirAsia is asked to pay a tax in the future, it can utilise the the tax credit, and save a lots of cash from the taxes it should pay.

My conclusion is, a "deferred tax" recorded in the income statement of a particular year actually bring no cash-flow into the company during that year. That's not an earning (at least in my opinion), just a future savings of tax. Showing the "deferred tax" in the income statement means recording a tomorrow cash-flow in today's statement. It's some kind of accounting technique to "polish" the financial performance of a company".

So, I've to do a new valuation on AirAsia. According to it's Q4-FY2007 statement, its EPSis about 21 sen, quite a good income. But if we exclude the deferred tax item from its income statement, its EPS is only 12 sen. If we exclude also the special item ("other operational income"), AirAsia's EPS for FY-2007 will become 8 sen only. This will give aPER value of about 25, quite a high number for a conservative investor like me. So, the share price of RM1.90 now is not as attractive as what i thought before.

However, the latest financial report shows that AirAsia still pose a very good prospect in the coming years. It's quite likely to have a 50% growth in PAT this year. So now... I'll hold its stock and continue to monitor its performance. If its EPS for FY-2008 (excludingdeferred tax) can grow to a value not less than 15 sen, I'll consider to keep accumulating AirAsia's stock.

22 October 2007

On Time Performance of AirAsia & other airlines.

one reason I think AirAsia will continue to growth is its great on-time performance. An airlines that has a consistent punctuality will win the customers' respect and build up its name, thus gain a bigger market share in long run.

In this article, I just want to show: how good actually is the the on-time performance of AirAsia?

Here's the figures I get from AirAsia's website:

* a flight is considered on-time if it departs no later than 15 minutes from the schedule time.

From the chart, its two months (Aug & Sep) average performance is about 88%, Three months average (Jul~Sep) is about 85%.

From the chart, its two months (Aug & Sep) average performance is about 88%, Three months average (Jul~Sep) is about 85%.We have to make a comparison to show how good is this figures. First, Lets compare the on-time performance of Jetstar Airways. (data from jetstar's website:http://www.jetstar.com/).

We can see that the on-time performance of AirAsia is as good as Jetstar's. And, Jetstar is the winner of the Best Low-cost Airlines (worldwide) in Skytrax's World Airline Awards 2007. I think this shows that AirAsia's performance is among the best in the world. (of cource, in this comparison, we assume that the figures announced on both airlines' website are true and reliable.)

We can see that the on-time performance of AirAsia is as good as Jetstar's. And, Jetstar is the winner of the Best Low-cost Airlines (worldwide) in Skytrax's World Airline Awards 2007. I think this shows that AirAsia's performance is among the best in the world. (of cource, in this comparison, we assume that the figures announced on both airlines' website are true and reliable.)Then, how about the comparisons with others airlines?

After some searching through the internets, I found that most Airlines do not publish theiron-time performance on their web-site. However, we can get some statistics fromhttp://www.flightstats.com/. Although the figures at this website only reflect the 20 most active routes for each airlines, it shouldn't be much different from the actual values.

Here's the figures I get from the website for some of the best airlines worldwide:

(statistic period: 15-Aug 2007 ~ 15-Oct 2007)

Low Cost Carriers:

| Air Berlin | 80% |

| easyJet | 80% |

| Jetblue Airways | 76% |

| Jetstar Airways | 81% |

| Southwest Airlines | 83% |

| Tiger Airways | 85% |

| Singapore Airlines | 84% |

| Thai Airways | 79% |

| Cathay Pacific Airways | 75% |

| Qatar Airways | 73% |

| Qantas Airways | 73% |

| Malaysia Airlines | 76% |

Unfortunately, the statistics about AirAsia at http://www.flightstats.com/ is incomplete, because it contains only figures for routes to Macau (which is about 65% on-time). This figures of single destination may be very different from the overall performance of AirAsia. For other routes which they don't have any data, they just quote 0% on-time-performance and 100% flight-cancellation. This does not reflect the real situation.

So, we can't double check the reliability of the on-time performance figures announced at AirAsia's website. However, according to my own experience (I've flown with AirAsia twice in September, and each flight I took depart on-time) and some of my friends' recently, I personally believe that error on the announced figures should be within 5%. So, lets assume that the real figure is 5% lower than the officially announced, the two-month-average performance of AirAsia (Aug & Sep-2007) still stand above80% (88% - 5% = 83%).

Conclusion: AirAsia on-time performance ranks among the best worldwide. Its performance is much better than those full service carrier like MAS, giving it an opportunity to grab a bigger market share in the future. I belive LCC model will continue to shake the aviation industry, and AirAsia will continue to grow and become the leading LCC in the reagion.

27 August 2007

How big is the brand "AirAsia"?

Some people around me always travel in flight due to their job. Hence, I'd heard a lots from them about AirAsia and MAS. And from their mouth, I know the conditions of the services and performances of these airlines.Here are my observations on the growth in AirAsia during these years:

One or two years ago, people still don’t like AirAsia. They choose AirAsia just because it is cheap. People has a lots of complains like:

Attitude of its staff were bad.

The food on flight is not good enough.

It doesn’t assign seat numbers for passengers.

Boarding onto AirAsia’s flight is a bit mess up, just like getting on a bus.

Delays and cancellations are common.

Some rumors said that AirAsia sometimes combined the passengers of two flights into one.

Actually, most of these negative impressions arise from people’s over-expectation on AirAsia to meet the same standard as other airlines, because most people that took AirAsia didn’t have any experience with other LCC. They can only compare AirAsia to their previous experience with normal airline, especially MAS. We all know that, MAS is famous (worldwide) for its good service and excellent attitude. (always, I heard that MAS flight attendances are all quite beautiful too). In fact, MAS wins the Skytrax's Best Cabin Staff Award for many years. So, the quality of AirAsia’s services is just too bad as compared to MAS.

while AirAsia is keep improving, people now gradually get used to AirAsia’s no-frill style – no ticket, no assigned seat, no free meal, etc.

An important improvement of AirAsia is the reduction of delayed flight. AirAsia’s on time performance for the past six months is about 85%. Some of my friends now prefer AirAsia than MAS, even when they are on an official trip (means they don’t have to pay for the air tickets, their employers will pay for them), simply because they are fed up with the (infamous) flight-delays of MAS.

Another reason they prefer AirAsia is that AirAsia makes their schedules more flexible, because it has a higher flight frequency than MAS. They have more choice for the departure time.

So now, the name “AirAsia” means a lots.

Besides my own observations, there are some supporting points that AirAsia is a greatbrand:

One or two years ago, people still don’t like AirAsia. They choose AirAsia just because it is cheap. People has a lots of complains like:

while AirAsia is keep improving, people now gradually get used to AirAsia’s no-frill style – no ticket, no assigned seat, no free meal, etc.

An important improvement of AirAsia is the reduction of delayed flight. AirAsia’s on time performance for the past six months is about 85%. Some of my friends now prefer AirAsia than MAS, even when they are on an official trip (means they don’t have to pay for the air tickets, their employers will pay for them), simply because they are fed up with the (infamous) flight-delays of MAS.

Another reason they prefer AirAsia is that AirAsia makes their schedules more flexible, because it has a higher flight frequency than MAS. They have more choice for the departure time.

So now, the name “AirAsia” means a lots.

- It means “cheap”. This is the most sucessful brand image for AirAsia. When I fly, I definitely choose AirAsia; because I know that with AirAsia I'm having the lowest fare.

- It also means “less delay”, as compared to MAS.

- It means “more choice” for departure time, due to its high flight frequency.

Besides my own observations, there are some supporting points that AirAsia is a greatbrand:

- In the new released World Airline Awards® year 2007, AirAsia ranks no.1 in Asia region for the Best Low-cost Airline Award. (The Skytrax’s World Airline Awards® are recognized around the world, and renowned for being the only truly global, Independent passenger survey of airline standards.)

- Recently, a new AirAsia Credit Card was launched. The issuer of this new AirAsia’s card is Citibank. As we know, Citibank is the top-brand in credit card service. Citibank is now partnered with AirAsia...... I think this means something.

- Couple of weeks ago, the Virgin’s Group announced that it’ll take up 20% in FAX. There are total five airlines under Virgin Group, each of them carry the word "Virgin" in their name, e.g. Virgin Atlantic, Virgin America, etc. But this time, instead of using its “Virgin” brand, FAX is renamed to "AirAsia X" to start its long-haul LCC business. As Tony said, “AirAsia brand is very big, bigger than Virgin out here.”

21 August 2007

Reasons of buying AirAsia

In value-investment, you must be able to list downs the attractive features of a company that you're investing in. If your text can't cover for (at least) half page of a paper, it's probably that you're not quite understand this company, and this investment can't be considered a secure one.

So, I decided to list down all the reasons for every company that I buy. I start with AirAsia, because this is my latest investment. I'm still quite excited that I found this company for investment.

I invest in AirAsia, because it's a great company, due to the following reasons:-

And I hope that my holding period for this stock is...... forever.

.

[updated 3/11/2008]: Months after holding AirAsia, I had found several accounting pitfalls in the statements of AirAsia. In short, AirAsia's performance is not as good as I thought before (i.e. when I wrote this post). For more details, pls refer to my other posts tagged "airasia".

.

So, I decided to list down all the reasons for every company that I buy. I start with AirAsia, because this is my latest investment. I'm still quite excited that I found this company for investment.

I invest in AirAsia, because it's a great company, due to the following reasons:-

- Simple business model that I can understand.

- A growing company in a growing industry.

- Great management – Tony Fernandes

- High profitability – It has a high profit margin compared to the other LCCs.

- Leader in the industry – Best Low-cost Airline Award (rank no.1 in Asia region), year 2007 .

- Strong Brand Name - high value of intangible asset.

- AirAsia's stock price is around RM1.80 today. 9-month profit for FYE2007 is about RM0.13 per share. this means its PER for 2007 is about 10 to 12.

- its 9-month revenue grow 53%, and the 9-month profit before tax grow 190% as compare to 2006.

- based on its growth in fleet size from 50 aircrafts (this year) to about 150 (year 2013), my estimation for its average growing rate in the next five years is about 25% per annum.

- The ratio of PE to its growth rate is less than 0.5, so the price may be considered cheap. (This is an analysis technic suggested by Peter Lynch).

- its net asset per share is just 64sen. This is less comfortable for a secure investment. But AirAsia has a great value of intangible asset - its brand name.

And I hope that my holding period for this stock is...... forever.

.

[updated 3/11/2008]: Months after holding AirAsia, I had found several accounting pitfalls in the statements of AirAsia. In short, AirAsia's performance is not as good as I thought before (i.e. when I wrote this post). For more details, pls refer to my other posts tagged "airasia".

.

14 August 2007

Discover the low-cost-carrier - AirAsia

The first time I heard about AirAsia, is from friends around me.

People start talking about AirAsia.

“AirAsia’s ticket is very cheap”,

“It’s a new airline, you can fly with only RM9.99”

“now flying to Penang is cheaper than driving”

wow, this company is really cool....

I love Airasia, because she makes “every one can fly”.

and She makes me able to fly.

Before the existence of AirAsia, I never fly. The air tickets are just too expensive. Being attracted by its “One Million Free Tickets” promotion and the low prices, I had been flying with AirAsia more than ten times during past twelve months. And because of AirAsia, I and my wife can have our honey-moon in Bali.

Thanks to AirAsia.

When flying with AirAsia, I found that it is almost full-loaded in every flight, especially during weekends. When the price is cheap, just about every one likes to take a flight.

So, some voices come into my mind,

“I like this company, she really makes every one fly”

“this company must be making plenty of $$$$$”

“Buy its share!”

A lots of people don’t believe in the business model of AirAsia.

“the air tickets are so…… cheap…..!!!!”

“how can it make profit out of that….???”

“the low price is just temporarily, it will raise the price later, or it may not survive”

“how long can it last before going to bankrupt?”

But for me, I believe in the magic of Wal-Mart:

The lower is your price, the more money you make.

And I really love the phrase sound: “the more you help people to save their money, the more $$$$ you get from them”

Wow, this is the greatest idea in the world. The feeling of “earning money while helping people to save money” is just like “getting rich while doing charity”. Sounds cool……

And, you know, AirAsia is doing the same thing as Wal-Mart. So, I decided study this company.

订阅:

评论 (Atom)